Top 3 Income Issues Slowing Your Closing | Blueprint

New Year’s is an interesting holiday to me. It is the only holiday that seems to prompt the most change in people’s lives. When you think about it, does anyone say, “This Thanksgiving I am going to start doing push-ups every day”? Some New Year’s changes occur whether you plan them or like them or […]

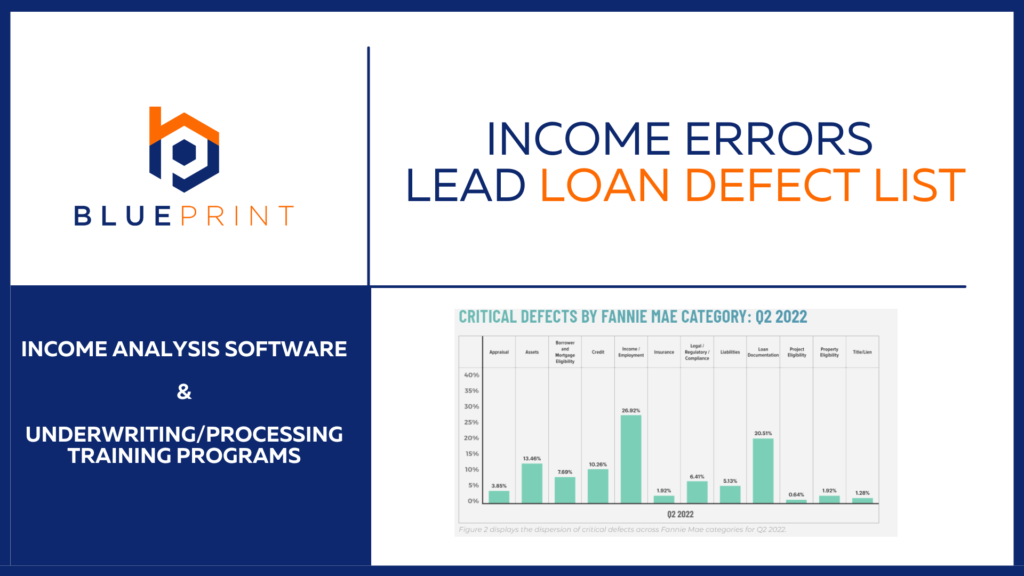

Income Defects

ACES reports income errors lead loan defect reasons 11th straight quarter When I write a blog headline, I try to balance the blog name between informative and relevant to give the reader a good idea of what the blog is about and a reason to click on it. Personally, I find too many articles today […]

Calculate Self|Employed Borrower Income | Blueprint

There are four steps on how to calculate income for self-employed borrowers. Borrowers who are self-employed have two distinct roles in the process of generating their personal income. Due to the dual nature of their daily roles of income generation and the higher risk, it can prove to be more challenging to determine their income […]

Can a borrower use K-1 income with under 25% ownership?

Can you use K1 income with less than 25% ownership? K-1 income(loss) is generated from standard business structures defined by the IRS which are Partnerships using the IRS 1065 tax form and the S Corp using the IRS 1120S tax form . These entities both use an IRS form K-1 as one of the ways […]

HOW TO DO A MORTGAGE INCOME ANALYSIS

One of the lessons I learned during my underwriting career is that the most likely reason a borrower defaults is due to their DTI ratio (Debt To Income), or stated in plain english you “can’t afford” the payment on your house. This is because the DTI either starts off too excessive or becomes too excessive […]

Freddie Mac Bulletin 2022-18

Freddie Mac Bulletin 2022-18 offers new method of income calculations for 1099 borrowers. The United States is looking at earning income much differently than it did just a decade ago. With industry mavericks like Uber changing the way Americans get around cities, they and other companies led the way into our new Gig Economy. The […]

FHA Mortgagee Letter 2022-09

FHA has recently amended their guidelines to allow more flexibility to calculate income for borrowers whose variable income was affected by the COVID 19 pandemic as announced in mortgagee letter ML 2022-09. FHA guidelines tend to focus on two years averaging of income, many borrowers were affected in the last two years due to COVID. […]

How to complete a liquidity test

When completing income analysis for self employed borrowers there are a few key steps that must be followed. A liquidity test must be performed before your borrower can use self employed income from a K-1 attached to a 1065 or 1120S tax form. How to complete a liquidity test? Follow these steps. Step one Make […]

K-1 Income For Self Employed

Calculating K-1 income for self employed K-1 income for self-employed borrowers is one of the most common questions we receive. We understand—it’s complicated. As mortgage professionals, we aren’t tax experts, but since self-employed individuals make up a significant percentage of potential borrowers, it’s crucial to understand how to calculate K-1 income correctly. Key considerations First, […]

Fannie & Freddie Drop P/L Requirements

As a person that has worked, trained, and mentored in the mortgage underwriting world for 27 years, I definitely guessed the profit and loss situation wrong! My best guess was at earliest they may remove the P/L after you filed your 2021 returns, but to my surprise the following happened. On February 2, 2022 as […]