ACES reports income errors lead loan defect reasons 11th straight quarter

When I write a blog headline, I try to balance the blog name between informative and relevant to give the reader a good idea of what the blog is about and a reason to click on it. Personally, I find too many articles today in all areas of life that have a shocking headline, then you read the article and there is a big nothing-burger following the shocking headline. For example, have you ever seen headlines like “Doctors give secret to losing weight overnight,” only to find out it says “sleep and drink water” in the article??

ACES Quality Management is a long time QC player in the mortgage world and highly respected. The MBA put out this news link from them that got our attention for good reason: ACES : Critical Defect Rates Up 6%. Unlike many articles online today, this one has real data with real lessons the mortgage business needs to heed.

I personally have been in the business since 1994, and what I have learned through the up and down cycles is this: When your mortgage business is busy, and shortcuts in training, systems, or QC work are not followed, it won’t be the slow months that cause you to close your doors. It will be paying for the bad habits when it was busy AND the lack of volume (i.e. PROFIT) to pay for the loose standards during the busy times that will close them.

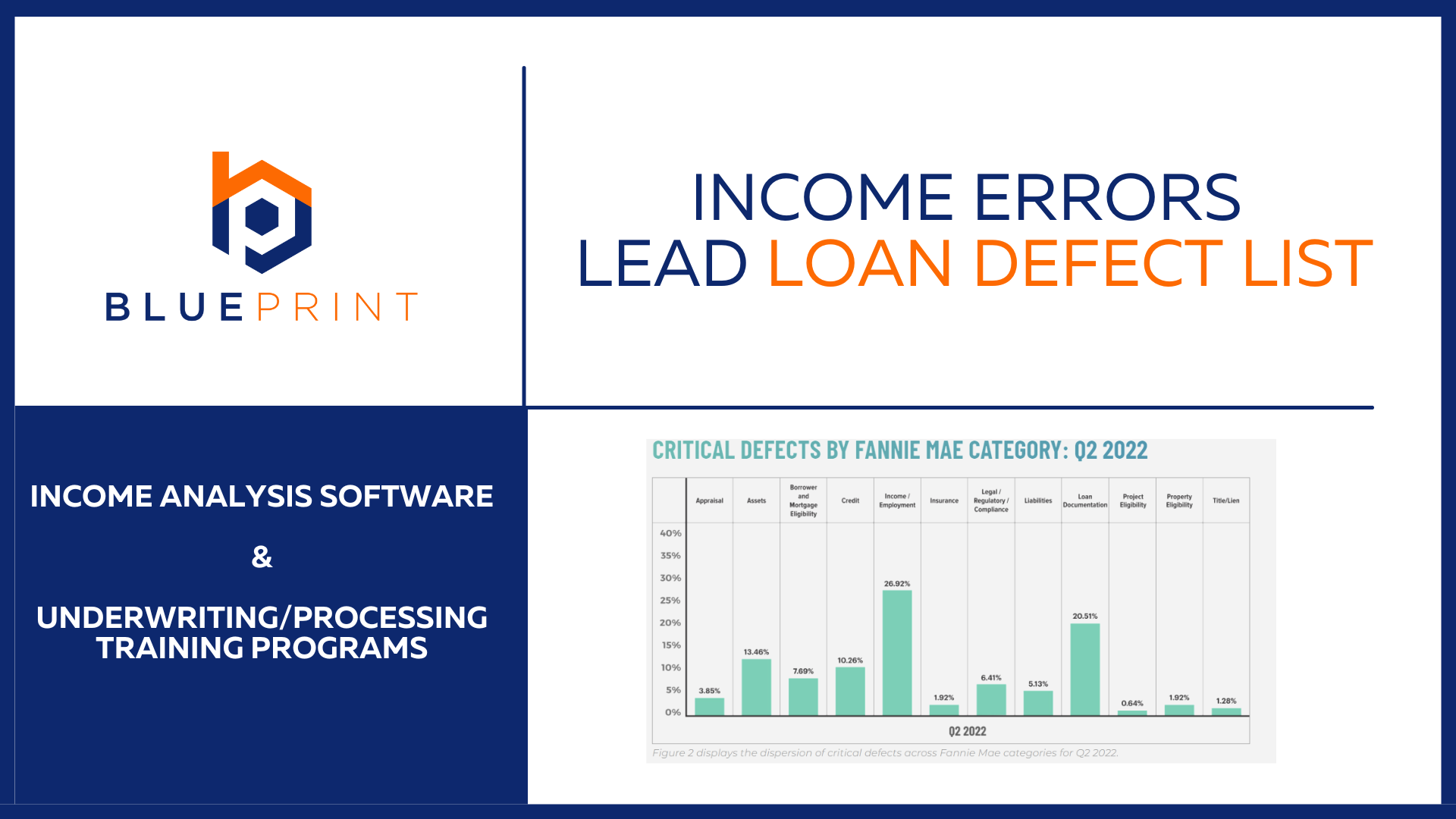

Reading down into their data, this quote jumped out at me (and the supporting chart):

While still the leading defect category for the 11th straight quarter, the Income/Employment category improved 21% over last quarter, comprising only 26.92% of all defects in Q2 versus 34.27% in Q1. Given concerns that this would be an area in which lenders may stretch the limits to help qualify borrowers, seeing a significant decline in this category puts some of those fears to rest. SOURCE ACES

What can we do about income analysis issues?

The income defect rates are a problem that Blueprint was formed to solve, and why we built our income analysis system IncomeXpert. IncomeXpert system is the engine that knows the rules, calculations, and trending analysis requirements to do the income right.

In the ACES report, their suggestion to lenders is to look at the areas with the highest error rates and place their focus there. I would like to elaborate on what “place your focus” would look like as a four-part system that will keep things turning.

Step 1: Train your team

Step 2: Let your team execute

Step 3: Audit the work executed

Step 4: Take the audit results and measure what did or did not work to adjust and improve

Let’s talk deeper out on step two. If your team is still using spreadsheets, form fills, and free online MI calculators, at BEST, those tools are limiting. And if you keep using them, the labor costs in underwriting will make income analysis challenging. Your team needs a modern solution to the income problem, not the decades old solution to the problem.

Here is one example of a better process for income evaluation. Our partner, Lender Tool Kit, has just launched PRISM, which is powered by IncomeXpert. This tool is a turnkey integration built into Encompass that will solve nearly all the issues you see in mortgage income analysis errors. Combine PRISM with PRISM PLUS and the integrated Encompass workflow and this is an easy to use, comprehensive income analysis system that is simple to learn and can be deployed FAST.

PRISM powered by IncomeXpert will:

- Show team members exactly what numbers to enter

- Provide easy to follow advisories on special fields, for example, non-recurring expenses

- Any income can be calculated with PRISM

- Safe and secure team collaboration inside of Encompass

I hope I have followed my own rule where the headline was interesting enough but followed up with information or an actionable step to make your mortgage business better.