Full QC on every loan

Every automation file is fully QC'd for accuracy

Hybrid automation

Manual vs. upload is your choice.

Upload tax returns

Automate your workflows

The challenge of communicating income calculations

Calculating income for your borrower can be quite challenging. But the bigger challenge in many cases, is explaining how the income was determined to another party. Keep in mind whatever method you use to figure out the income, it may be viewed by the investor, an auditing company, or an agency in the future. This could be in one week, one month, or one year after the loan was sold. With no formal requirements or guidelines on how to document the income, this creates variability and leaves you open to deficiencies in your income documentation.

Current Solutions

The solutions used by most mortgage companies fall into one of these categories.

- The underwriter puts notes on the 1008

- Use of basic spreadsheets to show the calculations

- Agency forms like the 1084, Form 91, or third-party form-fill sheets

Let’s go through these solutions to see which merits trust and which should be avoided in your loan analysis.

1008 Underwriting Notes

This is where many companies start off. Companies trust their underwriter with the task of uniformly and clearly explaining their income analysis and documenting their analysis in their own words. The truth is that underwriters are humans and humans can’t not be relied on for consistency. Underwriters try their best, but production requirements, interruptions, and limited space on the 1008 all cause issues with this approach.

During a typical audit review examples like this are very common. The scenario is that the borrower has two jobs, a schedule C business, and three rental properties identified. When the auditor reads the 1008 notes, the underwriter has entered this :

YTD income OK both jobs, using base, SCH C income steady , and rental income validated.

If the above statement is confusing to read, you are not alone. Keep in mind that statement is supposed to explain to an auditor the name of the income, the type of income, the calculation method, and there has to be some kind of breakdown of the income analysis to validate the final answer.

Conclusion: This method should not be trusted to sell loans on a secondary market

Spreadsheets

Spreadsheets are a major upgrade to the 1008 underwriting notes. There is no doubt about that. Where spreadsheets work best is borrowers with singular types of income. For example the borrower has one job, or one Schedule C, or one rental property. When you get a borrower that has multiple income types the spreadsheet struggles at clearly breaking down the analysis to explain how each income was determined. Many are not designed to evaluate and combine multiple sources of income.

Even with the best work arounds, the spreadsheet will always meet a loan scenario it was not designed to handle.

The second issue is that spreadsheets are prone to errors created by each user. Somebody using a spreadsheet does a cut-and-paste in the wrong spot and your formulas become corrupted. That same person unknowingly shares the spreadsheet with errors in it. Pretty soon as a company with 25 underwriters you could have many different versions of that same spreadsheet being used. If you work at a company that uses spreadsheets, is there a person in charge that audits the sheets for accuracy, controls versions, and validates the security is valid to avoid corrupting the formulas?

The third issue is that spreadsheets are not smart enough to recognize and follow the underwriting rules required for an accurate calculation. For example there are times that the underwriter must subtract mortgage, notes, and bonds from the income of a self employed borrower based on their percentage of ownership. But there are ways to leave that income that can be included, IF certain rules are checked (for example if line 1D SCH L from the business has enough cash to cover that debt). We call these rules “if / then” rules, which work like this. “IF” item A is true THEN do B, but IF item A is false THEN do C”. Spreadsheets simply are not great at multiple choice answers.

Some might say that they have macros, formulas, and protected fields to address these concerns. Those approaches are band aids for using the wrong tool for the job.

Conclusion: This method should not be trusted to sell loans on a secondary market

Form-fills and cash flow worksheets

To combat the problem of underwriting notes and the challenges with spreadsheets, vendors have come up with form fills, mainly focusing on the self employed borrowers These sheets have very severe limitations to them. The limitations are just like the spreadsheet and work best when you have one type of income and only one source of that income. Example if your borrower has three K-1 businesses these forms fall flat on evaluating each one but instead rely on a lump sum approach.

The form fill sheets are not dynamic. When you complete the sheets there are all kinds of blank boxes for unused incomes or income types, which is natural when you think of the one-size-fits-all method they are designed to address. They do not change information based on what investor or agency you are going to sell the loans to. They do not handle “IF/THEN” rules as described above.

The one advantage they do have over spreadsheets is that they are web based so the owner / creator of that form can control the versions. It would be very difficult to have a user corrupt the method of calculation, or for team members to use the wrong version of the sheet.

Conclusion: This method should not be trusted to sell loans on a secondary market

The IncomeXpert Report

The reason IncomeXpert was created was to create a better process of income evaluation, and our crown jewel is the income worksheet. We analyzed the problems in the audit of mortgage loans and found the industry needed a better income report to solve these issues.

- Accurate. Following guidelines for each agency regardless of the skill level of the user

- Complete. A single tool for all income types

- Clear. Three levels of income explanation: Overall Income, Summary By Type, and Detail By Type.

Our report meets all of those requirements. Our team threw away the typical industry approaches when we created IncomeXpert and started from scratch.

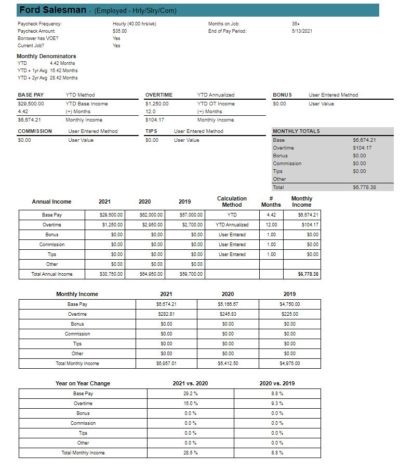

When you review the IncomeXpert report one of the things you will notice is that income is clearly documented and broken down. Your team won’t need a masters degree in financial analysis to follow the calculations used to determine the income.

The IncomeXpert report starts with the total income for each borrower. The report starts there because when a loan officer is trying to qualify a borrower they must know: how much does this borrower earn? The loan officer does not need a bunch of confusing totals and analysis, they need a bottom line.

The next section in the IncomeXpert report is the summary section. It breaks down each income by type. This allows teams to review and see how each income source contributes to the total borrower income in the prior section. This is just like the total borrower income but with each income is listed in its own summary table.

The last section breaks down a detailed analysis of HOW the income was determined, trending analysis, and any agency advisories that were triggered. At Blueprint we feel strongly that:

You can have the right answer but it’s not right unless you SHOW YOUR WORK

The IncomeXpert report meets all of the requirements the agencies have for income. More importantly, these calculations are done systematically on every loan, every borrower. Bottom line there simply is NO income report on the market that embodies all of these attributes.

Conclusion: This method CAN be trusted to sell loans on a secondary market

Conclusion

Your team has better things to do than create and maintain internal spreadsheets or write up income analysis narratives on 1008 forms. Your team needs a consistent and compliant tool that does the work for them. Underwriters are masters of evaluating risk, so give them the tools to make those decisions and save their time crunching numbers, remembering agency income guidelines, and documenting income.

Total Income System – IncomeXpert

If you are struggling with income, guideline compliance, and getting consistent income. IncomeXpert might be a solution to consider. We provide over 200 guideline checks, trending analysis, and a complete income analysis system for your organization.