Responsible use of AI in mortgage underwriting

Automated income analysis using artificial intelligence (AI) is an emergent tool suite for mortgage operations teams. As with all technology, it can be used properly as well as improperly. The responsible use of automated income analysis must be considered with the rollout of any new tool or technology.

What if it’s wrong? How do you handle loss of availability? What if you don’t agree with the answer? These are all good questions to ask of any technology. If I adopt this new technology, what other changes do I need to make to my workflow to make best and proper use of it?

Mortgage underwriting is a complex process that involves analyzing a borrower’s financial situation to determine their ability to repay a loan. One of the key components of this process is income analysis, which involves verifying a borrower’s income through various means such as tax returns, pay stubs, and bank statements. However, this can be a time-consuming and human error-prone task, which is why automated income analysis software is becoming increasingly essential for streamlining the mortgage underwriting process.

How can AI be used?

Automated income analysis software uses advanced algorithms, machine learned models, and data analytics to verify a borrower’s income quickly and accurately. This can help lenders make more informed decisions about a borrower’s ability to repay a loan and reduce the risk of compliance or error.

Before we get to the cautionary aspects of these new technologies, let’s review the benefits they can provide.

Time savings

One of the main benefits of automated income analysis software is its ability to save time and improve efficiency. With manual income analysis, lenders may spend hours or even days poring over documents and verifying income. With automated software, this process can be completed in a fraction of the time, freeing up lenders to focus on other tasks and reducing the time it takes to close a loan.

Automated income analysis saves time for mortgage underwriters by streamlining the income verification process. With manual income analysis, underwriters may spend hours or even days poring over documents and verifying income. In contrast, automated software can quickly verify a borrower’s income by analyzing data from various sources, such as tax returns, pay stubs, and bank statements. This can reduce the time it takes to verify income and free up underwriters to focus on other critical tasks, such as risk assessment and loan approvals. With automated income analysis, underwriters can work more efficiently and make faster, more informed decisions, ultimately leading to a smoother, more streamlined mortgage underwriting process.

Furthermore, time savings can be amplified by performing the automated income analysis at the moment documents are available. This means the underwriting department can focus on reviewing the resulting analysis rather than manually performing the analysis or placing orders for automated income analysis.

Classification and income identification

By using automation to scan the income documents, human errors of omission can be avoided. Automation can reliably sort through thousands of pages of tax return information to identify income sources. Having an underwriter miss a declining income source that is hidden in 1000’s of pages of self-employment tax return information is a compliance risk. Using automation for tedious human activities such as document identification and classification mitigates risk of human error.

Another benefit of automated income analysis software is its ability to provide more accurate results. Human error is always a possibility, and manual income analysis can be prone to mistakes or oversights. Automated software, on the other hand, uses rigorously tested software to verify income, reducing the risk of errors and improving the accuracy of the results.

Complex Underwriting

Automated income analysis can empower junior staff to handle complex underwriting scenarios by providing them with powerful tools and data analytics capabilities. With automated software, junior staff can quickly and accurately verify a borrower’s income, even in complex scenarios such as self-employment or multiple income sources. This can help reduce the workload for senior underwriters and allow junior staff to take on more responsibility and make more informed decisions. Additionally, by using automated income analysis software, junior staff can learn and develop their skills faster, which can help them grow into more senior roles in the future. Overall, automated income analysis can help empower junior staff to handle complex underwriting scenarios with greater confidence and accuracy, ultimately benefiting both the staff and the organization as a whole.

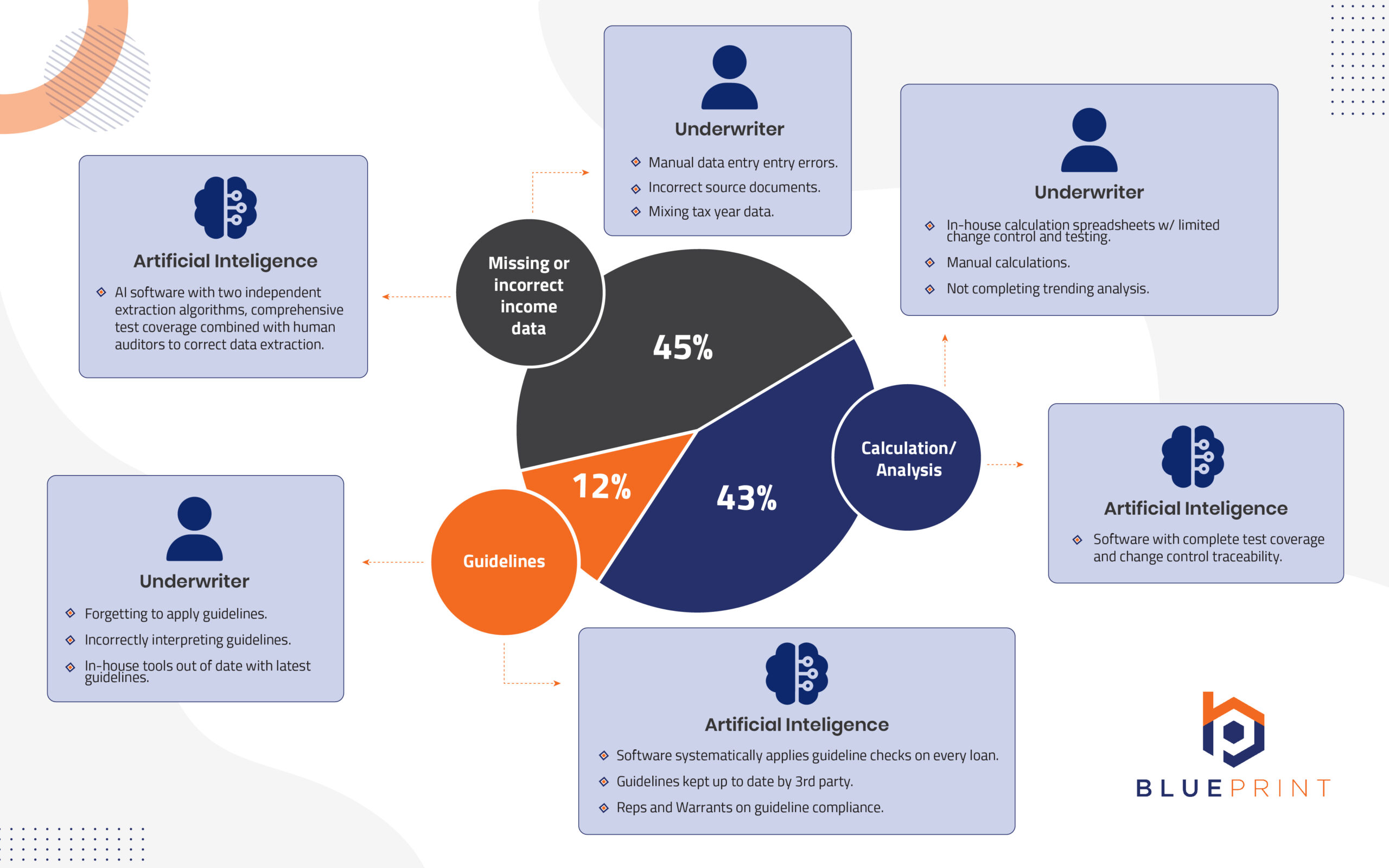

Reduced Miscalculation Rate

The term miscalculation is used extensively in mortgage lending. However, the reason for the miscalculation breaks down into three categories.

- Miscalculation due to arithmetic errors

- Miscalculation due to missing or incorrectly applied guidelines

- Miscalculation due to missing or incorrect information

Automation can drive down the miscalculation rate on all three of these categories. Software, even without the use of AI, can be developed to consistently calculate the correct values and apply the correct guidelines. The addition of AI enables the third and last improvement in miscalculation by enabling the identification of missing information.

Machine learning models are very well placed to inform you what is missing and to some degree, what is incorrect information. The expectation of a complete set of documents for a given tax year is set and machine learning algorithms can process through the entire document set to determine if everything is present and accounted for.

Risks of Artificial Intelligence

While the use of artificial intelligence in automated income analysis has many benefits, it is important to remember that AI is not infallible. Like all algorithms, AI can make mistakes or produce errors if it is not properly calibrated or trained.

Knowing where a technology has risk and weakness is essential to its successful adoption. Becoming over reliant on a technology with a minor deficiency can lead to downstream compliance risks in the mortgage space.

Savvy vendors who are adopting these technologies recognize this and implement safeguards to ensure the benefits of the technology are maximized and the risks are minimized. The following are the main risks lenders and vendors make when adopting advanced technology such as automated income analysis.

Not integrating product and process

By far, the number one risk people encounter in adopting any tool or technology is not integrating properly. Automated income analysis is no different in this regard. The tools and technology are not a process in and of themselves, they are tools to be used in an overall workflow your organization uses to fund a loan.

These advanced technologies are there to augment and support a human workforce executing a defined process. The technology is not there to define the process or replace the process.

Thus organizations need to think clearly when determining where in their current workflow the new tool or technology is inserted, what its inputs are, and what its outputs are before it is adopted. That sounds simple, but in practice it is the “did you think about” questions that will take your best laid plans and place them back on the drawing board.

Going deeper into the “did you think about” concept, let’s review the other risks in adopting advanced technologies.

Over reliance

Teams can implement a tool or technology, then become over reliant upon it and lose critical skills and expertise in the organization. It may be attractive to a middle manager to let all the expensive senior staff go and replace them with low-cost junior staff and augment them with advanced technology solutions. Financially, that may be attractive to some in management, but the savvy and pragmatic managers will understand the fallibility of the advanced technology and understand that we need experienced senior staff to help monitor and audit the outputs of these systems.

Not knowing the boundaries

As they say, garbage in, garbage out. These advanced technologies have boundaries, and failing to know them and monitor for deviations from these boundaries is a major compliance risk for your organization. It is very common to see cell phone images of income documents and tax returns. The warping, rotation, and scaling of these images pose a real risk to the downstream technologies expected to classify and extract information from these images.

While it is exciting to see these technologies handle examples of these tough to read documents, we need to recognize this as a risk and have human mitigations in place to support. Having policies to not accept these types of images is a great example of company policy mitigating risk for artificial intelligence systems in the organization. Submitting non-compliant images will require human processing and those submitting those types of documents can wait longer to get their results.

Handling downtime and availability

All computer systems experience some degree of downtime or loss of availability. Does your organization have backups to handle this? Manual processing for the times when systems may be down is a great solution, but only if you have engineered your team, processes, and tools to be able to function when the advanced technology isn’t available.

Failing to change how you audit

As we explore these risks, it underscores why it is critical that human auditors monitor the output of AI systems and verify the accuracy of the results. Organizations must audit the AI output, just like you audit a human staff member. The requirement to audit does not go away with the adoption of advanced technologies. What is often overlooked is changing how audits are performed in light of the use of AI systems and where their known weaknesses lie.

The big change here for AI auditing versus human auditing, is with humans you sample a percentage of their work to see if you detect any issues. If issues are found you can follow your action plan to correct those findings. This process is never ending and humans can be spot on one month and the exact same income the next month can be all wrong.

Auditing Remediation

Auditing remediation looks at random error vs. systematic error. If a human makes a mistake, is it a fluke, or is it because they are lacking knowledge or awareness of a guideline? Having a conversation with your co-worker can reveal which of the two cases may be true. But if you experience an artificial intelligence error that conversation isn’t as easy. Auditors need to take a different approach to addressing audit findings rooted in artificial intelligence errors.

The best practice here is to treat all artificial intelligence errors as if they were systematic errors, until you can prove otherwise. What does that mean? It means if you find that an artificial intelligence system failed to apply a guideline or incorrectly extracted a number from a tax return you must start with the assumption that it has done this before. Thus the auditor needs to forensically look for the same income types or loans where that guideline would be applied to determine if the artificial intelligence correctly functioned.

What complicates this is the technology may be ever changing and what was previously performant, might now be a regression in performance. Thus the dates and revision number of the artificial intelligence system become key data points to the auditor to root case and issue and determine if it is random or systematic. It might be that your audit uncovered a newly emergent degradation in performance due to a recent change in the system.

Robots vs. Humans

Underwriters and processors need not fear the introduction of automated income analysis solutions. Pragmatic uses of this technology increase the efficiency and accuracy of the human workforce they support. In other words, much like the adoption of the adding machine didn’t replace the need for accountants; underwriters and processors can leverage this technology to do more with less and drive down human error.

Some may use Artificial Intelligence (AI) solutions as a replacement for manual underwriting. The pragmatic application of this technology would not apply technology as a replacement, but rather an augmentation to the human staff. Thus lenders should be wary of solutions that are lacking the following:

- The ability to audit the Artificial Intelligence output

- The ability to modify or override the output

- The ability to know when to include or exclude data from income documents

As mentioned above, the requirement of auditing doesn’t change with the adoption of new tools, however the way audits are conducted and where auditors focus their efforts must be refined to ensure fallibility of artificial intelligence systems are considered.

Human Oversight

When the underwriter or auditor does find something that is incorrect, does the tool or technology allow them to change or override? Underwriting isn’t always black and white. There are risk decisions the underwriter needs to be able to make that can alter the final income analysis. Automated income analysis systems are best positioned to provide the safe minimum income and allow underwriters to increase the income by making risk decisions backstopped by guideline compliance checks.

A great example of this would be child support income. The income analysis may be easy but to qualify the income the underwriter has to take additional risk analysis steps. The risk steps are first checking the age of the child the support is for to confirm it will last for three years. The next step is to confirm the receipt of the child support on time and the correct amount for six months. These are the items that without additional context, artificial intelligence can’t make those determinations.

What’s the answer?

Automated income analysis software is becoming increasingly essential for streamlining the mortgage underwriting process. By reducing the time it takes to verify income and improving the accuracy of the results, this software can help lenders make more informed decisions and reduce the risk of compliance error. As the mortgage industry becomes more competitive and complex, adopters of these technologies need to be cautious and carefully implement processes and workflows that leverage the benefits of artificial intelligence while creating safeguards against the risks.